White eggs: a carbon claim laid over a price story

Published on : 8 Jun 2026

White eggs have been here before, and not always as a value product...

Sainsbury’s white egg announcement is not a ban on brown eggs. It affects the retailer’s own-label range, not the branded fixture: shoppers who want brown can still find it, but may have to step out of the own-brand range and into a branded pack.Happy Egg, from Noble Foods, sits outside the decision and remains the UK’s best-selling brand; other branded providers will keep offering brown depending on their listings, and Waitrose and Morrisons have both said brown stays in their ranges. So this is a narrowing of choice within Sainsbury’s own brand, not the end of the brown egg — a choice within own-brand becoming a choice between white own-brand and brown branded, or a reason to shop elsewhere.The carbon framingSainsbury’s presents the move as a sustainability decision: white eggs match brown on taste and nutrition while carrying a lower carbon footprint, with welfare benefits because white-feathered hens eat less feed and stay productive longer.The headline figure is a 12.7% lower carbon footprint per kilogram of egg from white birds than brown. SAC Consulting carried out a life cycle assessment on Sainsbury’s 2024 egg supply, covering hatchery, rearing, laying, packing and transport to shelf, and attributed the saving mainly to feed efficiency and the longer productive lifespan of white hens.That number, however, is not a universally accepted industry benchmark. Carbon footprinting depends heavily on the assumptions, datasets and boundaries used in the calculation: change the feed data, the flock assumptions, the treatment of land use change emissions or the calculator itself, and the result can look very different. The sector is some distance from agreeing a single methodology, which is one reason producers are wary of treating any single percentage as settled fact.Nobody disputes the birdFew producers dispute the modern white bird’s performance. White birds eat less feed — the biggest cost in the system — and are routinely taken longer in lay, commonly to around 100 weeks, against the brown-bird ADAS cost-of-production model, the industry standard, traditionally built on a shorter cycle nearer 86 weeks. But that benchmark is itself a moving target: not long ago ADAS costings assumed a 72-week end of lay, and the figure has crept up year on year. The brown bird is getting more efficient and lower carbon too — so a white-bird saving measured against today’s brown benchmark is judged against a baseline that keeps improving, and may move again before any comparison is settled.The economics follow directly: spread the pullet cost over more eggs and use less feed, and both the cost per dozen and the carbon number fall. On paper, the white bird has obvious attractions — and that is the heart of the matter. The debate is not about whether the bird performs, but about how the carbon claim is being presented.BFREPA, the British Free Range Egg Producers Association, has been more cautious than the retailer’s press line, noting that ADAS is still developing the white-bird costings needed to compare properly with the established brown-bird model. Without those cost assumptions in place, the carbon cannot be measured accurately either. ADAS costings are the sector’s gold standard, relied on by retailers, packers and producers for years; the white-bird equivalents are still being built as flocks reach end of lay. Sainsbury’s may have a figure for its own supply chain on its own assumptions, but the wider industry comparison has not been completed by the same route.Comparison is not straightforward in any case. White pullets cost more, feed intake differs, and margin turns on selling price, end-of-lay values, seconds and quality. White birds throw more seconds, and white eggs are harder to keep clean than brown — which matters under the new egg marketing guidelines. Nor do the downsides stop there: end-of-lay values for white hens are almost non-existent, the birds carry less meat and are flightier and harder to catch — all of which feed the true cost and the welfare picture, and none of which surfaces in a headline carbon number.Most producers do not recognise the 12.7% figure, and the arithmetic shifts with how it is built. Annualise the costings — spreading cost and output across a standard year — rather than running them to flock age at depletion, and both cost and carbon per egg look materially different, because much of the white bird’s advantage comes precisely from being kept longer in lay. In short, the carbon figure has reached shoppers before the industry has finished the costings that would let anyone judge it.White eggs are not new — and not always cheapWhite eggs have been here before, and not always as a value product. Noble Foods trialled them over a decade ago as Snowy Whites under the Happy Egg banner for Christmas, then launched Happy White Eggs in Tesco and Morrisons. The white shell was presented then as visually distinctive, even premium — not as the cheap egg.There is a longer history here, and it does not flatter the white egg. In previous incarnations, white eggs struggled whenever eggs were plentiful: retailers could not shift them and packers ended up moving producers back to brown. The lesson the trade drew was simple — given a genuine choice, shoppers reach for brown. That is what makes a full own-label switch different from merely adding white to the range. Removing the brown choice guarantees those white flocks a home, which may be exactly what sustains white producers while supply is tight — but it is a fragile basis for a permanent change. Let eggs return to abundance and give shoppers a real choice again, and the preference for brown reasserts itself: the white market narrows, and Sainsbury’s could be left committed to producers whose eggs shoppers would rather not buy. The nearer-term risk is sharper still — an own-brand egg shoppers do not want, while the brown one they do want sits on a competitor’s shelf a short trip away, Waitrose and Morrisons among them.The same shell colour has been discussed at the other end of the market, as a way to flag barn production on shelf as retailers sought a colony replacement. Major retailers committed to removing caged shell eggs by the end of 2025, effective from 1 January 2026 — not a legal ban, but it has already reshaped the fixture. The legal position is still moving: the Government has consulted on phasing out enriched colony cages, with the industry expecting any decision to point to a ban on existing colony systems by 2032.The shell colour is no longer just a barn marker in theory — white has become the barn staple in practice, the standard bird for the lower-cost, non-cage range retailers turned to once they rejected the cage. That complicates any premium reading of the white egg. The same shell Sainsbury’s wants to carry a carbon story is, across the aisle, the everyday value egg; and a colour already doing duty as the cheap barn workhorse cannot easily be dressed up with an elevated claim — carbon or welfare — at the same time.Sainsbury’s is therefore moving in a market shaped by the cage-free deadline, the likely colony ban and the search for a cheaper colony replacement. Free range cannot replace colony like-for-like: modern units are smaller and more capital-intensive, built around an average 32,000-bird flock, not the large colony houses that served the value end. Planning is now one of the biggest brakes on new capacity — ammonia rules, nutrient neutrality, protected catchments and permitting have made development far harder, confining most new building to Yorkshire, Scotland and Northern Ireland, while in parts of England and effectively across Wales producers say permission has become almost impossible.Retailers still need eggs. They need British eggs, cage-free eggs, lower-carbon eggs — and eggs at a price shoppers will pay. White birds help because they are efficient, barn because it is cheaper than free range. Put those pieces together and the attraction is obvious.The suspicion on farmSainsbury’s presents the move as a carbon decision. Many producers believe cost and margin are playing at least as large a role, and that those advantages existed long before carbon became the headline. The suspicion in parts of the industry is straightforward: a commercial saving is being dressed up as an environmental breakthrough.White eggs are cheaper to produce. Whether that saving lifts producer returns, cuts shelf prices, or stays elsewhere in the chain is unclear — and there is little sign shoppers will see a cheaper egg because own-label is going white. The market is tight, the cage transition continues, and new free range capacity is hard to build. The white birds themselves are scarce: producers report they cannot get white chicks until 2028, so the switch cannot be scaled at pace even if the will were there. With supply that constrained, retailers have little reason to drop prices simply because the bird is cheaper to run — nobody marks down an egg they are struggling to source. The likeliest outcome is that the saving is captured somewhere other than the till.There is a contractual dimension that sharpens the point. Many producers are on fixed prices set against the only costing the industry has — the brown-bird ADAS model — some locked for three or four flocks ahead. Those prices cannot simply be cut, and there is no agreed white-bird costing to renegotiate against. Anyone wanting to bring egg costs down runs straight into contracts built on brown numbers — which makes a switch to a bird with no established costing all the more convenient, sitting outside those contracts and reopening the price conversation. The ground has shifted in the producer’s favour, too: under the government’s Fair Dealing regime — in force for milk and pigs, with egg regulations promised within two years — producers will for the first time have recourse to the Agricultural Supply Chain Adjudicator if a purchaser backtracks on a contract.There is a strategic risk in the timing. The industry cannot publish costings to order — the white-bird figures are still being built as flocks reach end of lay — but the longer the gap between commercial decisions and completed numbers, the more producers react to figures set by others. Whoever puts the first credible cost saving on the table sets the reference point, and an embedded number is far harder to argue down than to anchor. Should retailers judge the saving larger than the industry’s benchmarked data supports, that higher figure drives the price conversation — leaving producers firefighting after the event rather than negotiating from an agreed baseline.That the market will reward the cheapest egg, whatever its credentials, is already being proved elsewhere. Tariffs on Ukrainian goods were suspended after Russia’s 2022 invasion; most products now run tariff-free to 2029, but eggs and poultry were singled out as the sensitive exception, kept on a shorter leash and recently extended again from April 2026 to March 2028. The effect has been stark. The UK barely imported Ukrainian eggs before 2022, yet took close to 12,000 tonnes of Ukrainian shell egg and product in the first ten months of 2025 alone, against a pre-war quota of around 400 tonnes a year; imports have roughly doubled since 2021, and about one egg in nine in retail is now imported, most of it Ukrainian. That success rests on nothing more sophisticated than price — no carbon calculation, no life cycle assessment on the pack, much of it cage production long banned here — and buyers, particularly in food service, take it because it is cheap. Producer bodies call it a plain double standard: the same government preparing to ban enriched cages at home is holding the door open for eggs from cage systems outlawed here for over a decade, produced to lower welfare, environmental and food-safety standards than British law demands. British farmers carry the cost of those standards; their Ukrainian competitors do not. If the market rewards the cheapest egg regardless of how or where it was produced — and regardless of the welfare rules it would have broken on British soil — it is hard to argue a domestic shift to white birds is driven by anything but the same logic. Carbon is the story told on the shelf. Cost is the story told at the tills.

The instability is not confined to one database, nor to the latest standards...

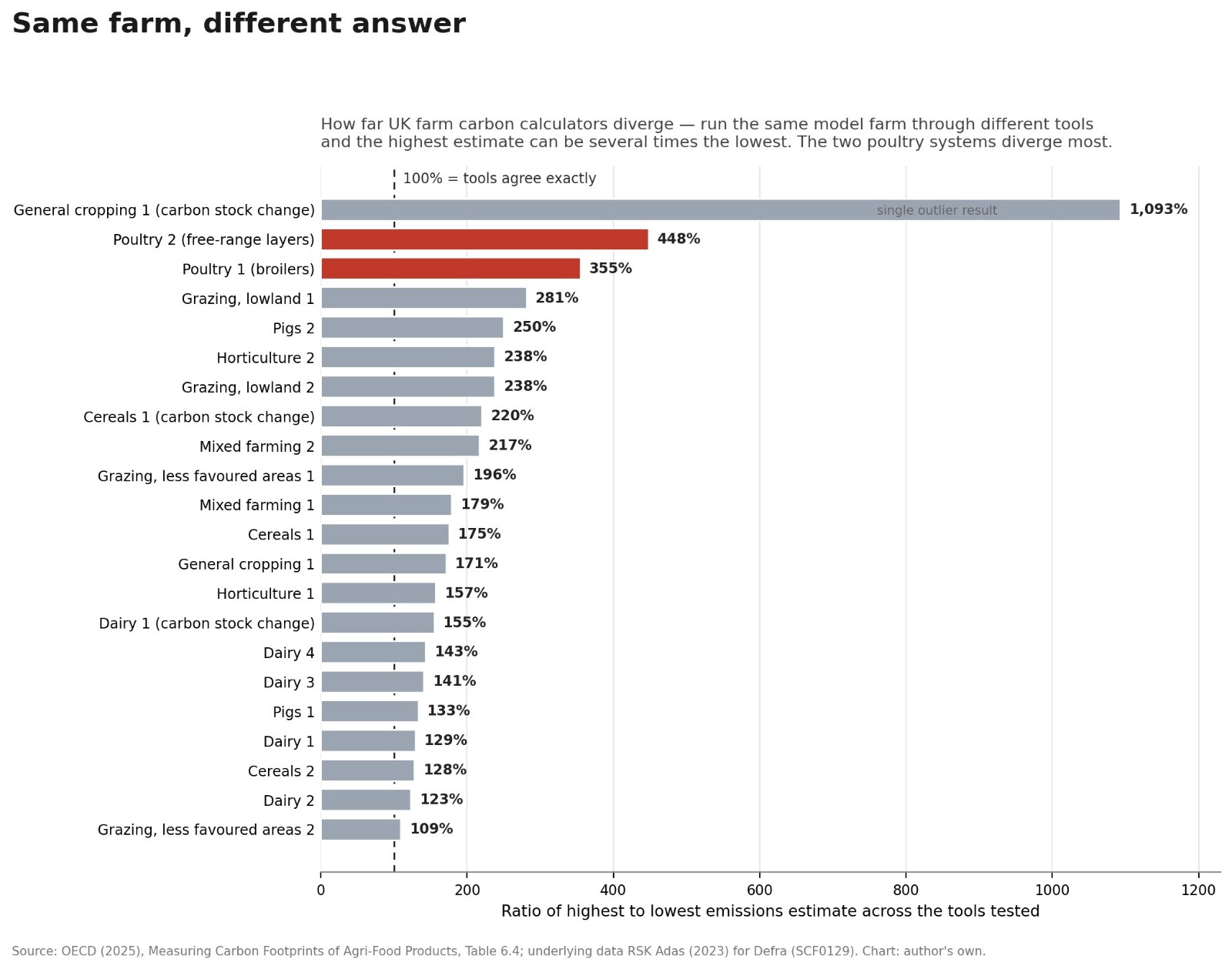

Why the carbon number can’t carry the weightTom Willings, director of strategy and partnerships at Eggbase, addressed exactly this at VIV Europe in Utrecht, in a World Poultry Science Association session titled Footprint to Foodprint. He argued that carbon measurement on poultry farms remains imperfect and that meaningful change needs co-operation across the value chain. His phrase captured the mood: the economic climate is overshadowing the environmental climate.Willings was not dismissing footprinting — Eggbase does it, and the principle that you cannot manage what you cannot measure holds. His point was reliability, the “moving goalposts” facing anyone building a carbon strategy. Take the GFLI database, the global reference for feedstock impact data: its version 3, published this year, cut reportable land use change emissions for Argentine soybean meal by more than 70% and Brazilian by more than 40%, while raising those for UK-grown beans more than a hundredfold. Several “sustainable” egg brands were built on soy-free, home-grown bean diets — under one version of the database that lowers their footprint, under the next it raises it. How can anyone plan to a reduction target when the figures move that far?The instability is not confined to one database, nor to the latest standards. Sainsbury’s 12.7% rests on an SAC Consulting assessment carried out to PAS 2050:2011 — a standard the AHDB now describes as outdated for farm-level carbon accounting, and which DEFRA’s own harmonisation work says carbon tools should move beyond. And when DEFRA reviewed the calculators available to UK agriculture in 2024 (report SCF0129), it found 81 different tools and, running 20 model farms through them, recorded enormous divergence — a 356% spread in results for broilers and a 448% spread for free-range layers. Same farm, same birds, same eggs; wildly different answers depending only on which calculator was used. And the field keeps multiplying: an OECD count Willings presents alongside that review shows the number of active carbon tools worldwide growing by around 90% in five years. Against that backdrop, a single, precise-looking percentage should be treated with caution whoever publishes it, because the choice of tool can swing the result further than any real difference between two flocks.The same problem sits behind the white egg claim. Sainsbury’s 12.7% may be perfectly valid inside its own assessment boundary, built on good data — but it is the answer that one boundary, one feed dataset and one set of flock assumptions produce, and an equally defensible set could move it. BFREPA is building its own layer-specific approach with Alltech E-CO2 precisely so producers can be measured consistently against peers — a programme growing fast and now covering around 100 flocks across both layers and rearers.Eggbase puts a sharper number on it. Eggbase, the poultry-specific tool that has footprinted large numbers of flocks across different packers, models the white bird’s carbon advantage not as a fixed number but as an indicative range of around 6 to 8% — and even that assumes the long 100-to-110-week cycle and higher egg numbers. That is roughly half the saving on Sainsbury’s sustainability page, offered as a band, not a decimal. More telling is where the bird sits in the order of carbon levers: on Eggbase’s reckoning the bird is worth perhaps 6 to 8%, a lower-land-use-change diet and tighter feed efficiency more than 20%, renewable energy and tree planting less than 1%. Feed is several times the lever shell colour is. A retailer genuinely chasing carbon would change the diet, not the bird — and the lever Sainsbury’s chose is the visible one that also happens to be cheaper to run.Willings flagged a deeper gap: feed is the biggest variable in any footprint, yet many farmers do not know exactly what is in their rations or where it comes from. Feed companies guard their formulations — and increasingly supply their own ration emissions, which, Eggbase notes, often come out lower than when calculated independently. With feed routinely over 80% of an egg’s footprint, the single biggest number is in effect marked by the party with most to gain from a low one. Sourcing decisions sit with mills, packers, retailers and procurement, not the farm, so a farm-level footprint can sit far from supply-chain reality — and a lower-carbon egg cannot be demanded of the producer unless the rest of the chain shares data, carries cost and rewards improvement.Peter van Horne, the egg economist, sharpened it: if a business sources feed from North rather than South America purely to lower reported emissions, does the planet gain, or has the problem just moved? A chain can improve its number without cutting global emissions. Eggbase sees the same from the bottom up: a producer can be the least efficient in a group yet post a better footprint simply because the soya came from the United States rather than Brazil or Argentina — origin can mask performance entirely. The same caution applies to white eggs: a retailer can improve its figure by changing the bird, the cycle or the supply mix. Producers want to know whether the reduction is real, consistent and fairly measured — or partly a function of where the boundary was drawn.

Several low-carbon egg brands have launched recently...

Carbon has never sold eggsSeveral low-carbon egg brands have launched recently; some are already gone, and the survivors lean on organic or welfare credentials rather than carbon alone. The clearest precedent is Morrisons, in 2022 the first UK supermarket to put a carbon-neutral own-label egg on shelf — its Planet Friendly range, from hens fed insects reared on the retailer’s own food waste, carbon neutrality verified by the University of Cambridge, carrying a BSI Kitemark and a green British Lion stamp. Even with that assurance it stayed a niche line, not a fixture-wide switch, and it sold on a vivid, tangible story — insect-fed, soya-free, food-waste-reared — not a bare percentage. That is the pattern: where a carbon egg has worked at all, it worked as one strand of a richer welfare or provenance story, never as the headline.What moves egg buyers is well established, and carbon is not on the list. Price, freshness and welfare top survey after survey: more than half of British shoppers say they always buy free range and a further quarter do so regularly, and the free-range share of retail eggs has risen from roughly a third two decades ago to about seven in ten today. Eggs are a cheap, habitual, weekly buy, decided in seconds on price, date and the familiar welfare cue — exactly where an abstract carbon claim has least pull. Net Zero has also slipped down the agenda as the cost-of-living crisis bites, and recent experience suggests carbon alone has never been a strong proposition. Sainsbury’s is asking customers to accept a major own-brand change on the back of one.The framing carries a regulatory edge. The Advertising Standards Authority has spent recent years tightening the rules on “carbon neutral” and “net zero” claims, after its research found consumers barely understood the terms and felt misled once offsetting was explained; it has banned food-sector ads it judged unsubstantiated, and the trade press notes there are still no agreed methodologies governing how such schemes are calculated. The Competition and Markets Authority now has powers to fine misleading claims up to 10% of global turnover. A 12.7% figure the industry has not agreed, used prominently to justify removing choice, sits squarely in the territory the regulators are policing.There is a reputational risk in the framing itself. Consumers are not naive, and a growing number can spot a margin decision dressed in environmental language. With households still squeezed by the cost-of-living crisis, presenting a cheaper-to-produce egg as sustainability — while offering no cheaper dozen and removing the brown egg most prefer — invites exactly the backlash starting to surface. The suspicion that a green claim is really a margin grab is corrosive precisely because it is plausible; a retailer seen to profit under a sustainability banner during a squeeze risks the goodwill the banner was meant to buy.British shoppers have long preferred brown eggs. White were common here until the early 1970s, before brown came to read as more natural. There is no nutritional difference, but preference has always mattered in the fixture, and national newspaper polling during this debate suggests around eight in ten still prefer brown. If so, Sainsbury’s is not merely helping shoppers choose greener; it is removing the own-brand version of the egg most would pick. As Willings put it in 2014, free range and colony fortunes sat “as on a see-saw with price differential at the fulcrum.” Shell colour may be the visible row. Price is still the fulcrum.The bottom lineThere is no need to pretend white eggs are inferior. Modern white birds are productive, persistent and efficient, and they may well become a bigger part of the British market. But Sainsbury’s has chosen to frame an own-brand switch around carbon before the industry has finished the white-bird costings and before layer carbon benchmarking has settled into a common language.The white bird appears to offer both a lower reported footprint and a lower cost of production, but where that saving ends up — with the producer, the shopper, or the supermarket — is still unanswered. The 12.7% may be neat enough for a sustainability page, but it is one model’s answer, not the industry’s.The white egg may be lower carbon. It is certainly cheaper to produce. Until the methodology is agreed and the costings completed, many producers will keep asking whether this is a carbon story at all — or a commercial one wearing a green label for a supermarket struggling to source eggs.Source: DEFRA review of agricultural carbon calculators (SCF0129)This article was first published in Ranger magazine as either a comment piece or news story. It is reproduced for reference only and should not be taken as representing the views of BFREPA unless expressly stated.